If you’re being audited by the IRS on cryptocurrency transactions, you may receive something you’ve never seen before: a form asking you to identify—under penalties of perjury—every digital asset platform, wallet, and service that you’ve ever used.

We recently obtained a copy of this form, issued to a client in an active IRS crypto audit. It’s entitled “List of Digital Asset Platforms, Wallets, Services, and Products Used (Individual Taxpayers),” (“HDAF Form”) .and it may represent a significant escalation in how the IRS is approaching cryptocurrency examinations.

Here’s what this form looks like, how the IRS is using it, and why responding to it without professional guidance could create serious problems.

What Is the IRS Historical Digital Asset Form?

This is not a publicly numbered IRS form like a 1099-DA or Schedule D. It’s not an OMB form, vetted and approved by the Federal Office of Management and Budget. It’s an examination document—a two-page attachment sent directly by IRS revenue agents during crypto audits. Based on what we’ve seen, it’s being issued by the Small Business/Self-Employed Division, and it requires taxpayers to disclose and attest to their lifetime history of digital asset activity.

The form we reviewed was sent as part of an Information Document Request (IDR) with a hard deadline of roughly four weeks to complete, sign, and return.

What the Form Asks For

The form is divided into three parts, and it casts a very wide net.

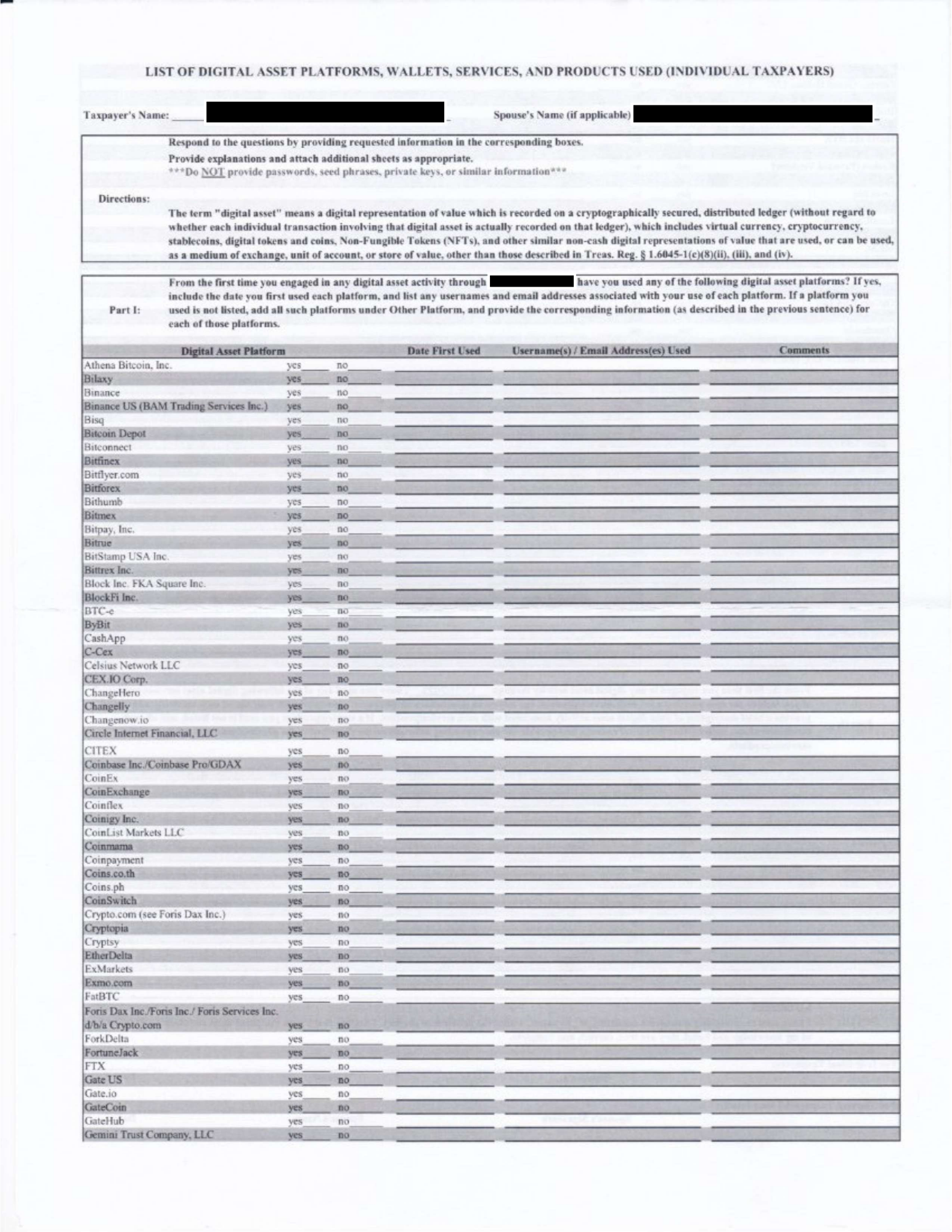

Part I: Digital Asset Platforms (Exchanges)

Part I contains a pre-printed list of over 100 cryptocurrency exchanges and trading platforms. This isn’t a short list—it covers virtually every major (and many minor) exchanges that have operated over the past decade. The platforms listed include well-known names like Coinbase, Binance, Kraken, Gemini, and Robinhood Crypto, as well as dozens of lesser-known or now-defunct exchanges like Mt. Gox, FTX, Celsius Network, BitMEX, and HotBit.

For each platform, the taxpayer must indicate whether they used the platform (yes or no), the date they first used it, and any usernames or email addresses associated with their account. As exhaustive as the HDAF form is, it asks tor the taxpayer to volunteer information not specifically requested by the checklist of platforms—there is also a “Comments” column, as well as blank rows labeled “Other Platform” for anything not otherwise listed.

The form specifies a look-back period. And the look-back period is….forever. In the version we reviewed, the taxpayer was asked about activity from the first time they engaged in any digital asset activity through 12/31/2023 (at least there is an end date, but that is only because the 2023 year is being audited). That means this isn’t just about the tax year under audit—the IRS is trying to map out your entire crypto history.

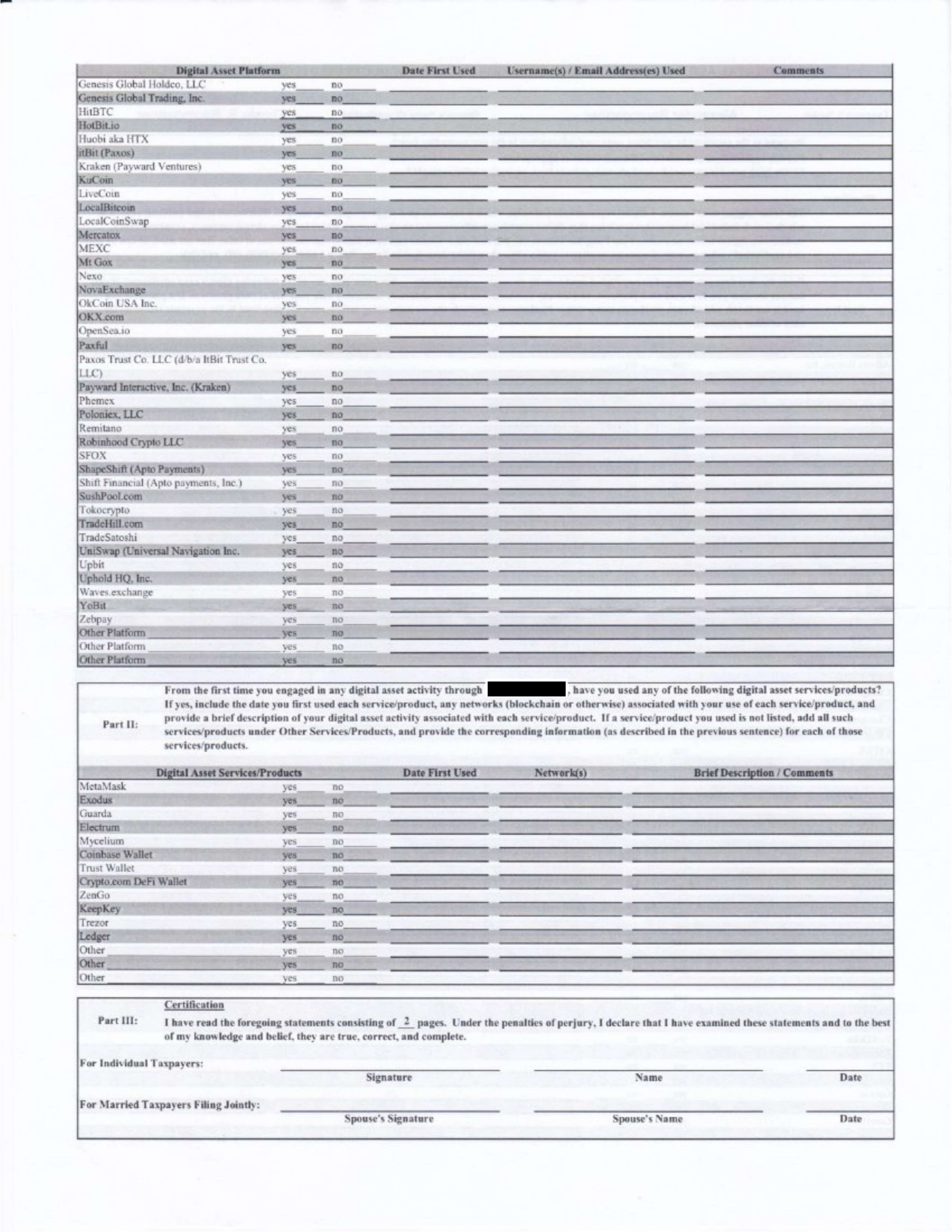

Part II: Digital Asset Services and Products (Wallets & DeFi)

Part II shifts the focus from exchanges to wallets, DeFi tools, and other crypto products. It lists popular self-custody wallets and services including MetaMask, Exodus, Ledger, Trezor, Trust Wallet, Coinbase Wallet, Electrum, Mycelium, and others.

For each service or product, the taxpayer must disclose whether they used it, the date they first used it, any associated blockchain networks, and a brief description of the digital asset activity associated with the product. This section also includes blank “Other” rows.

This is notable because it shows the IRS is now specifically probing DeFi and self-custody activity—not just exchange-based trading. If you’ve used MetaMask to interact with DeFi protocols, bridged tokens across chains, or held crypto in a hardware wallet, the IRS wants to know about it.

Part III: Perjury Certification

This is the part that should get your attention. Part III is a certification statement requiring the taxpayer (and spouse, if they filed jointly) to sign under penalties of perjury. The language states: “I have read the foregoing statements consisting of 2 pages. Under the penalties of perjury, I declare that I have examined these statements and to the best of my knowledge and belief, they are true, correct, and complete.”

Let that sink in. The IRS is asking taxpayers to swear, under penalty of perjury, that they have fully and accurately disclosed every crypto platform and wallet they have ever used. This isn’t just paperwork—it’s a statement with legal consequences. The inclusion of the oath raises the stakes significantly. Swearing to something under penalties of perjury is often the difference between a misdemeanor 26 U.S.C. § 7207 charge, and a felony 26 U.S.C. § 7206(1) charge. More importantly, if the misrepresentation of historical crypto activity does not result in an underpayment, no felony evasion charge is possible, given an evasion charge’s required element of a “tax due and owing”. See 26 U.S.C. § 7201. But 26 U.S.C. § 7206(1) (false statements and returns, also a felony) requires no element of an underpayment or deficiency—what it does require is a false statement submitted under oath. Long and short, falsely attesting to this form would technically support a felony charge under 26 U.S.C. § 7206(1)—even if the year under audit was resolved with no underpayment of tax.

How the IRS Is Likely Using This Form

This form is a strategic tool for the IRS. Here’s what we believe they’re doing with it.

Cross-referencing with third-party data. The IRS has been issuing John Doe summonses to cryptocurrency exchanges like Coinbase, Kraken, Poloniex and others for years. They also receive 1099-K, 1099-B, and (starting in 2025) 1099-DA data from brokers. By asking you to self-report your exchange usage, the IRS can cross-reference your answers against data they already have. If you answer “no” as to a platform where you actually had an account, that’s a problem.

Building a complete transaction map. Crypto traders frequently move assets between exchanges, wallets, and DeFi platforms. The IRS has historically struggled to track this activity because on-chain transactions are pseudonymous. This form essentially asks the taxpayer to fill in the gaps—providing the IRS with a roadmap of everywhere their crypto has been, and when it was there.

Identifying unreported income and hidden assets. If a taxpayer discloses wallets or exchanges not reflected on their tax return, that opens the door to further examination. And examinations of other tax years. Similarly, if the taxpayer fails to disclose a platform the IRS already knows about, it raises red flags about intentional concealment.

Creating a perjury trap. The perjury certification elevates this from a routine information request to something with teeth. If the IRS later discovers that a taxpayer failed to disclose a platform or wallet on this form—even inadvertently—they have a signed, sworn statement they can use to support penalties or even criminal referrals.

The Risks of Responding (and of Not Responding)

This form creates a catch-22 for taxpayers.

Inadvertently missing a platform is a real risk. Many crypto users—especially those who were active in 2017 through 2021—signed up for dozens of exchanges and wallets over the years. Some of those platforms are now defunct. Some were used once and forgotten. Some operated under different names (for example, Crypto.com was formerly known as Foris Dax Inc., and Kraken’s parent company is Payward Interactive). The form lists over 100 platforms, but the crypto ecosystem has included thousands. Forgetting just one—especially one where you had a small balance or made a few trades—is entirely possible, and yet you’re certifying completeness under perjury.

Disclosing too much can open new lines of inquiry. Every platform for which you check “yes” becomes a potential source of further IRS requests. The examiner may issue summonses, request additional records, or ask you to reconstruct transactions for platforms that weren’t part of the original audit scope.

Not responding isn’t a great option either. Failure to cooperate during an audit can lead the IRS to issue a summons, propose adjustments based on their own records, or lack thereof (which may be less favorable to you), or assert additional penalties for non-cooperation.

What You Should Do If You Receive This Form

Do not sign and return this form without consulting a tax attorney or experienced crypto tax professional. This isn’t an exaggeration—the perjury certification alone makes this a document that requires careful review and consideration before you respond.

Here’s what we recommend:

- Engage a crypto tax attorney immediately. A tax attorney can communicate with the IRS on your behalf, manage deadlines, and help you craft responses that are accurate without being unnecessarily expansive. Attorney-client privilege also protects your communications in a way that working with an accountant alone does not.

- Reconstruct your crypto history before responding. Pull records from every exchange you can access. Check old emails for sign-up confirmations. Use blockchain explorers and crypto tax software to trace wallet activity. The goal is to build as complete a picture as possible before you sign anything.

- Consider the scope of disclosure carefully. Your attorney can advise you on what the IRS is legally entitled to and how to respond to the form in a way that’s truthful and protective of your rights. There may be legitimate reasons to negotiate the scope of the request or push back on certain aspects of the form.

- Request an extension if needed. The HLDAF form that we reviewed had a roughly four-week deadline. That’s a tight turnaround for a document of this significance. Your representative can request additional time from the revenue agent.

A New Front in IRS Crypto Enforcement

This form signals that IRS crypto audits are becoming more sophisticated and more aggressive. The agency isn’t just asking for your Coinbase Form 1099 anymore—they want a comprehensive account of every platform, wallet, and DeFi product you’ve touched, going back years. Years that are not even under audit. And they want you to swear to it, under penalty of perjury.

We’re continuing to monitor how this form is being used across different IRS divisions and audit types. If you’ve received this form—or any IRS correspondence related to your cryptocurrency—contact us. We handle crypto tax audits and IRS disputes nationwide.

Need help with a crypto tax audit?

Gordon Law represents taxpayers in IRS cryptocurrency audits, including examinations involving the new Historical List of Digital Assets form. We’re a crypto tax law firm that handles complex IRS disputes, from Schedule D discrepancies to unreported exchange accounts.

Contact Gordon Law to schedule a consultation.