For noncash charitable contributions to a 501(c)(3) organization, taxpayers often need clarification about the rules and regulations surrounding the deductions they can claim on their taxes. One area of confusion is the requirement for a qualified appraisal for cryptocurrency contributions.

In this post, we’ll explore the answers to two important questions recently addressed in an IRS Memo 202302012:

- Is a taxpayer required to obtain a qualified appraisal for contributions of cryptocurrency for which they claim a charitable contribution deduction of more than $5,000?

- If a taxpayer is required to obtain a qualified appraisal but fails to do so, can the reasonable cause exception apply if the taxpayer determines the value of the cryptocurrency based on the value reported by a cryptocurrency exchange?

Let’s dive into the details.

Charitable Deductions for Donated Cryptocurrency

Here is the scenario: You have done quite well investing in crypto, and decide to “give back” by donating a fair amount to a worthy 501(c)(3) organization. Generally, when donating appreciated property to a charity, you are not limited by your cost basis when calculating the charitable deduction, provided that you have held the property for more than one year (long-term capital gain property). So, the primary reason you wish to donate the crypto itself (rather than selling the crypto and donating the proceeds) is because you have owned the crypto for more than a year—you bought it for a lot less than what it is worth at the time of donation, and you do not want to pay a large capital gain on its sale.

You know what the crypto is worth – you can pull your smart phone out of your pocket and see that the 5 bitcoin that you donated to, for example, Doctors Without Borders, were worth $530,000 on the day you make the contribution. And that worthy charity sells the 5 bitcoin the very next day for something very close to $530,000, and uses that money to proceed with its good work. And so, you think, I will simply claim a charitable deduction for $530,000 on my tax return. Right?

“No good turn should go unpunished”— Oscar Wilde.

Without more , the IRS is probably going to deny the deduction. First, it’s important to note that under Section 170(f)(11)(C) of the I.R.C., a taxpayer must (in most circumstances) obtain a “qualified appraisal” for any charitable contribution of non-cash property for which the taxpayer claims a deduction of more than $5,000, including contributions of cryptocurrency.

If a taxpayer fails to obtain a qualified appraisal, can they still claim the deduction if they determine the value of the cryptocurrency based on the value reported by an exchange? Or by the value the charity places on the donated crypto? Probably not.

Although a qualified appraisal is not required for donations of certain “readily valued property”—which category includes “publicly traded securities” (stocks, bonds, debentures, etc.), and while some cryptocurrencies might be considered to be publicly traded securities, the prudent thing to do is regard the crypto as something other than a “readily-valued public security” for these purposes— even though one can determine (to the penny) just how much the crypto was worth at the time it was donated. Similarly, even though the charitable organization will probably determine the value of the crypto donated and inform the taxpayer what it regards as the FMV of the crypto donated, and even though that valuation will probably be spot-on, the charity is not considered to be a “qualified appraiser” that can authoritatively determine the value of the crypto.

So, if a taxpayer claims a charitable contribution deduction of more than $5,000 for a contribution of cryptocurrency, he or she should obtain a qualified appraisal, AND file with the return IRS Form 8283 – a form that summarizes the non-cash contribution. The appraisal should be obtained prior to the due date, including extensions, for the filing of the return. If the donation is $500,000 or more, you must also attach the qualified appraisal to the return itself – not just the Form 8283.

If you don’t have a qualified appraisal for the property you’re donating, you might still be able to prevail in your claim for a tax deduction. The important things that you must demonstrate are that there was a good reason for not obtaining the appraisal (usually, that reason turns on your reliance on professional tax advice) and that you made the donation in good faith.

If you’re considering making a charitable contribution of cryptocurrency, you should consult a tax professional to understand the rules and regulations surrounding the deductions you can claim.

Our experienced tax lawyers can help you better understand the deductions you qualify for. We can also put you in touch with a qualified appraiser whose valuations of the donated crypto will stand up to IRS scrutiny.

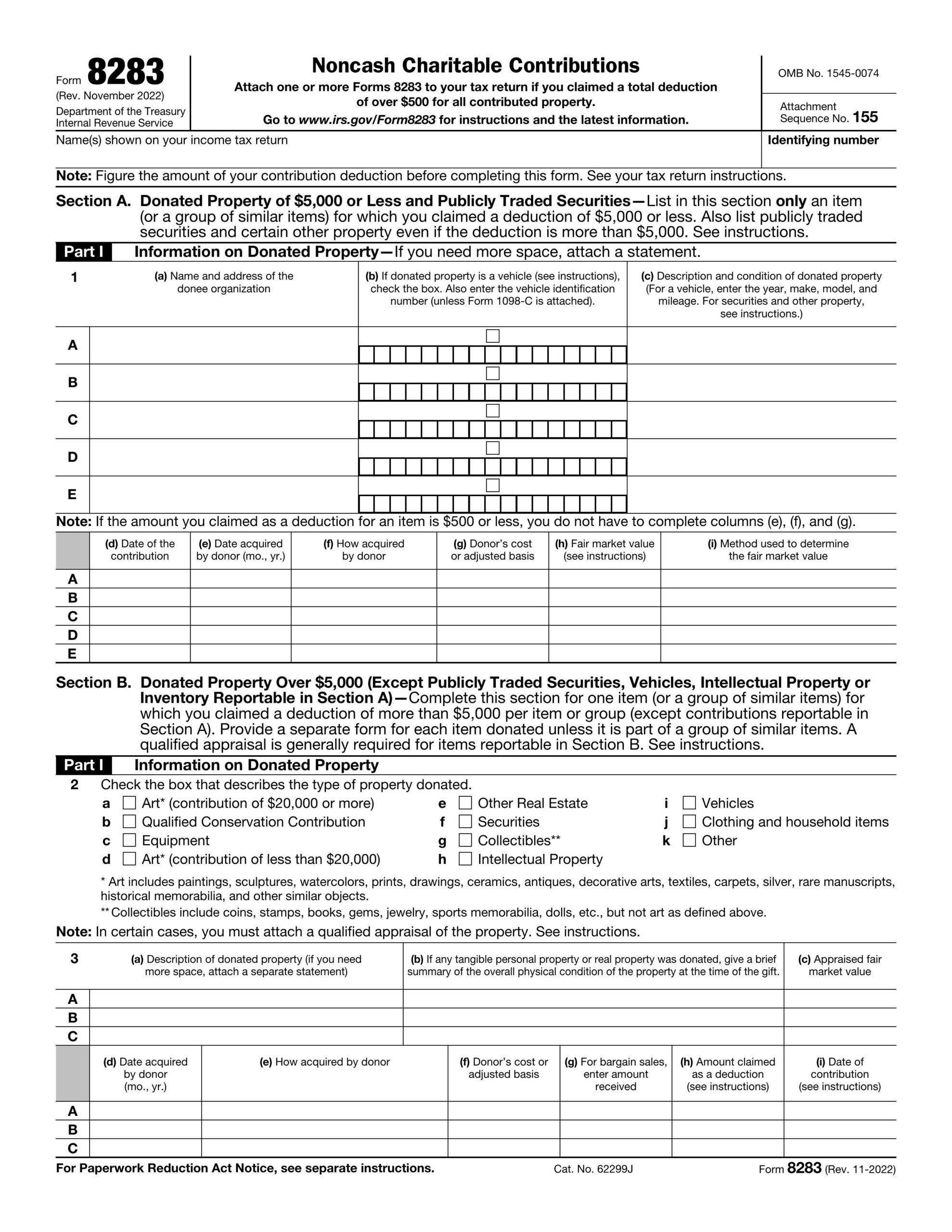

What is IRS Form 8283?

IRS Form 8283, also known as the Noncash Charitable Contributions Form, is used to report noncash donations of property worth more than $5,000 to charitable organizations. These donations include:

- Clothing

- Household items

- Cryptocurrency & NFTs

- Artwork

- Real Estate

For donations worth more than $5,000, the form must be completed and attached to the donor’s tax return. It includes sections for the donor to provide information about the donation, such as a description of the property and its fair market value.

It also includes a section for the charitable organization to provide a statement of the organization’s use of the property and any restrictions placed on the use of the property. For noncash donations valued at more than $5,000, a qualified appraiser must complete the appraisal and attach it to the form.

It is also important to note that the IRS has specific rules regarding the deductibility of noncash donations.

For example, if the donor has used the property for more than one year, the deduction is generally limited to the property’s fair market value. However, the deduction may be more significant if the charitable organization has used the property in furtherance of its tax-exempt purpose.

Need Help With Donated Crypto?

In light of recent developments in the tax treatment of donated cryptocurrency, taxpayers need to understand the requirements for claiming a deduction.

If you’re thinking about donating your crypto, it’s important to know that you can claim a tax deduction. However, there are specific rules that you need to follow, like getting a special report called a “qualified appraisal.