As a foreign-owned U.S. corporation or foreign company doing business in the United States, you’ll likely have to file IRS Form 5472, “Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business.” It is a crucial document for international tax compliance, and we’re here to help you understand it with this comprehensive guide.

Form 5472 is complex, and multinational tax laws can be challenging to navigate for someone without professional competence in this field. We recommend filing this document with a tax professional with focused experience in international taxes to avoid penalties, dissolve confusion, and ensure compliance. At Gordon Law, we leverage our extensive experience in offshore tax filing to make your organization’s tax season simple and stress-free.

In this guide, we’ll take a deep dive into IRS Form 5472, touching on key topics like filing requirements, example scenarios, due dates and deadlines, filing instructions, and potential penalties.

What Is Form 5472?

Form 5472, “Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business,” is an IRS form that aims to keep an eye on U.S. corporations with significant foreign ownership, as well as foreign companies doing business in the United States.

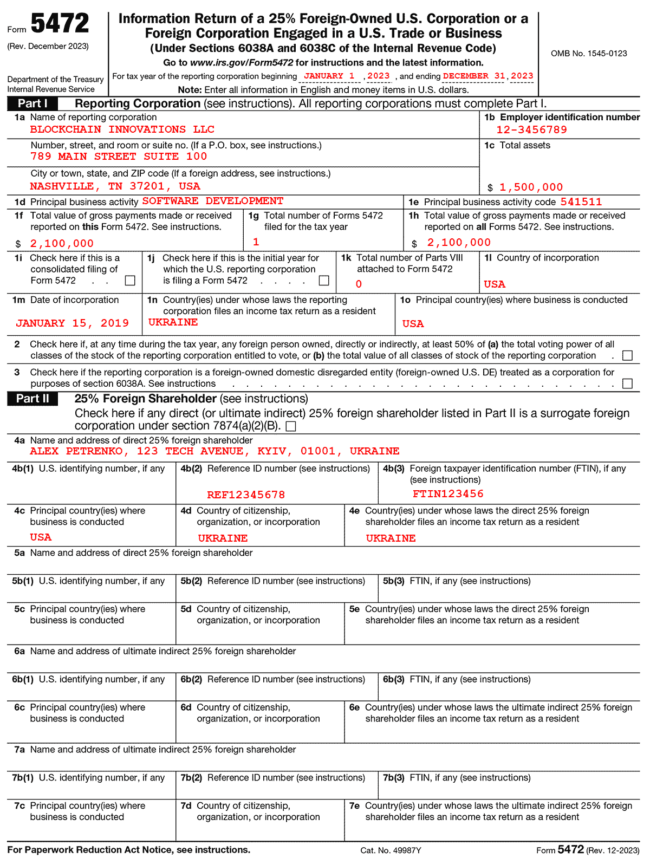

Below is Page 1 of IRS Form 5472 completed with sample information. Click to see a larger image.

The main purpose of Form 5472 is for the government to monitor the flow of transactions between reporting entities and related parties. This ensures compliance with U.S. tax laws and helps combat financial crimes like money laundering and tax evasion.

Form 5472 is an information return that likely won’t impact how much taxes your company has to pay.

What Is the Difference Between Form 5471 and Form 5472?

There is a key difference between Form 5471 and Form 5472:

- Form 5471 is generally filed by a U.S. taxpayer (either a person or a business entity) with at least 10% of ownership in a foreign corporation,

- While Form 5472 is filed by U.S. companies with 25% foreign ownership, foreign businesses engaged in a U.S. trade or business, and U.S. disregarded entities wholly owned by a foreign person.

Form 5472 Filing Requirements: Who Needs to File?

Form 5472’s filing requirements apply to your organization if it falls into any of the following three categories:

- 25% foreign-owned U.S. corporations: U.S. businesses with at least 25% foreign ownership and a reportable transaction must file Form 5472. According to the IRS, a corporation is 25% foreign-owned if it has at least one direct or indirect 25% foreign shareholder at any time during the tax year.

- Foreign corporations engaged in a U.S. trade or business: In case they are involved in reportable transactions with a related party, foreign corporations engaged in a trade or business within the United States are also subject to Form 5472’s filing requirements. Under Form 5472, a related party refers to the reporting corporation’s direct and indirect 25% foreign shareholders and other persons related through control or ownership.

- Disregarded entities: U.S. disregarded entities (DEs) fully owned by a foreign person must also file Form 5472, even if they are not obliged to file income tax returns. A disregarded entity is a business entity that has a single owner (e.g., a single-member LLC) and has not elected to be taxed as a separate entity for federal tax purposes.

Exceptions

Some exceptions from filing may apply to Form 5472, such as:

- Your organization had no reportable transactions for the tax year. We will explain what is considered a reportable transaction on Form 5472 later in this article.

- The related company qualifies as a foreign sales corporation for the tax year and files Form 1120-FSC. However, this exemption doesn’t apply to foreign-owned U.S. disregarded entities.

- Your organization is a foreign corporation with no permanent establishment in the U.S. under an applicable income tax treaty, and files Form 8833.

- A U.S. person controlling the foreign related corporation files Form 5471 to report information under Section 6038. However, this exception doesn’t apply to foreign-owned U.S. disregarded entities. The U.S. person must complete Form 5471’s Schedule M and provide details about all reportable transactions between the reporting corporation and the related party for the tax year.

The above are a few common exceptions; the rest are listed in the IRS’ instructions for Form 5472.

However, international tax laws are complex, and you shouldn’t necessarily be the one filing offshore tax forms like Form 5472. Instead, consider hiring an experienced international tax lawyer for minimum stress, maximum accuracy, and optimal results.

Example Scenarios

Below, we have listed a few example scenarios to better understand who has to file Form 5472 and in which cases:

- Company A is a startup owned by its two co-founders, who are both U.S. citizens. By the end of the tax year, they raise funding from an angel investor in London who now holds a 30% stake in the organization. As a UK citizen, the new investor is a foreign owner with over 25% ownership in the startup and multiple reportable transactions with Company A, which would make Company A subject to Form 5472’s filing requirements.

- Company B is a car manufacturer based in Germany. It is a well-known brand with a presence in the United States, which it considers one of its key markets for vehicle sales. Since Company B is a foreign corporation engaged in a U.S. trade or business, it would need to file Form 5472 for the tax year.

- Company C is a U.S.-based LLC treated as a disregarded entity for U.S. tax purposes and owned by an Australian citizen. As a domestic disregarded entity fully owned by a foreign national, Company C would be required to file Form 5472.

Form 5472 Due Date and Deadline

Form 5472 must be filed with the reporting corporation’s yearly income tax return (Form 1120) by the return’s due date each year the organization meets the filing requirements. The deadline for Form 1120 is the 15th day of the fourth month after the end of the business’ tax year.

For example, if your business’ tax year ends on December 31, 2024, Form 1120 and Form 5472 would be due by April 15, 2025.

However, one exception applies. Corporations with a fiscal tax year ending on June 30 must file the form by the 15th day of the third month after the tax year’s end (September 15). You can learn more about tax return deadlines on this IRS page.

Optionally, you can file a six-month extension for your corporate tax return to postpone the filing deadline for both Form 1120 and Form 5472.

Pro Tip: Foreign-owned U.S. disregarded entities must also file a pro forma Form 1120 with Form 5472 attached by the same due date, even if they don’t have an income tax return filing obligation. While they can request a six-month extension via Form 7004, foreign-owned U.S. disregarded entities can’t file their tax returns electronically. Instead, they must fax or mail the documents to the IRS.

What Is Considered a Reportable Transaction?

Under IRS Form 5472, a reportable transaction includes any monetary and non-monetary exchanges between the reporting corporation and related parties. These cover a wide range of transactions, such as:

- Inventory and tangible property sales and purchases

- Platform contribution and cost-sharing transaction payments (paid and received)

- Royalties, rents, loan guarantee fees, interest, and insurance premiums (paid and received)

- Sales, purchases, leases, and licenses of intangible property rights

Refer to Form 5472 for the full list of transactions.

Form 5472 Penalties: What Happens if You Don’t File?

The IRS imposes a penalty of $25,000 per form per year when the reporting corporation fails to file Form 5472 by the due date or fails to maintain records. The same fine applies to a substantially incomplete Form 5472, which the federal agency considers a failed filing.

If the failure continues for over 90 days after the IRS’ notification, the reporting company will have to pay an additional $25,000 penalty.

In addition to a fine, criminal penalties under Sections 7203, 7206, and 7207 may also apply if the reporting company fails to submit the required information to the IRS or files false or fraudulent information.

Pro Tip: Worried about potential Form 5472 penalties? Work with a team experienced in international taxes at Gordon Law to stay clear of IRS fines and make your tax season stress-free.

Form 5472 Instructions: How to File?

Follow these steps to file Form 5472:

- Gather the Necessary Documentation: To get started, collect all the necessary information, financial records, and transactional details about the reporting corporation and any domestic or foreign related parties. Examples of the documentation may include contracts, ledger entries, invoices, and loan agreements.

- Complete the Form: Fill in all nine parts of Form 5472 accurately, providing all the required information. Make sure to include all reportable monetary and non-monetary transactions in Part IV, Part V, and Part VI.

- Attach to Tax Return: Next, attach Form 5472 to your corporation’s annual tax return (Form 1120 for U.S. corporations and Form 1120-F for foreign businesses).

- Review and Submit the Form: Carefully review the form to ensure accuracy and prevent mistakes, and submit it with your corporation’s annual tax return by its respective due date.

- Seek Professional Guidance: International forms are complex, leaving much room for human error. To avoid penalties and ensure accurate filing, consult an international tax lawyer.

- Keep Records: You should keep records of your filed Form 5472, tax returns, and supporting documents for potential IRS inquiries and future reference.

Pro Tip: In case your organization has to amend its yearly income tax return (Form 1120-X), it must also attach an amended Form 5472 to reflect changes in reportable transactions.

Need Help Filing Form 5472? Gordon Law Makes it Easy

Filing Form 5472 and other offshore tax forms can cause headaches for those without focused experience in international tax laws. That’s why we’re here: to help you navigate these challenges and relieve you from the anxiety that typically comes with the tax season.

At Gordon Law, our team leverages its extensive experience in international tax laws to ensure accurate and compliant filings for your company. Contact us for a peace of mind in all your tax matters!