If you’ve ever invested in crypto, you probably know the harsh reality of watching the market plummet before your eyes. But there may be a silver lining to those market dips: depending on your portfolio, crypto tax loss harvesting may save thousands or even millions of dollars on your tax bill.

Crypto tax loss harvesting is a way to avoid capital gains tax without damaging your portfolio. If you realize enough losses, you can even offset the capital gains earned in future years.

Here’s what you need to know about this powerful money-saving strategy!

What is Crypto Tax-Loss Harvesting?

Crypto tax loss harvesting is a powerful way to save money on taxes, especially at the end of the year or during a bear market.

Are you holding onto cryptocurrencies or NFTs that have lost value since you bought them? Then you’re sitting on unrealized losses. With crypto tax loss harvesting, you can sell specific assets at a loss in order to lower your tax bill.

Tax loss harvesting brings multiple advantages when used correctly. Depending on your holdings, you may be able to:

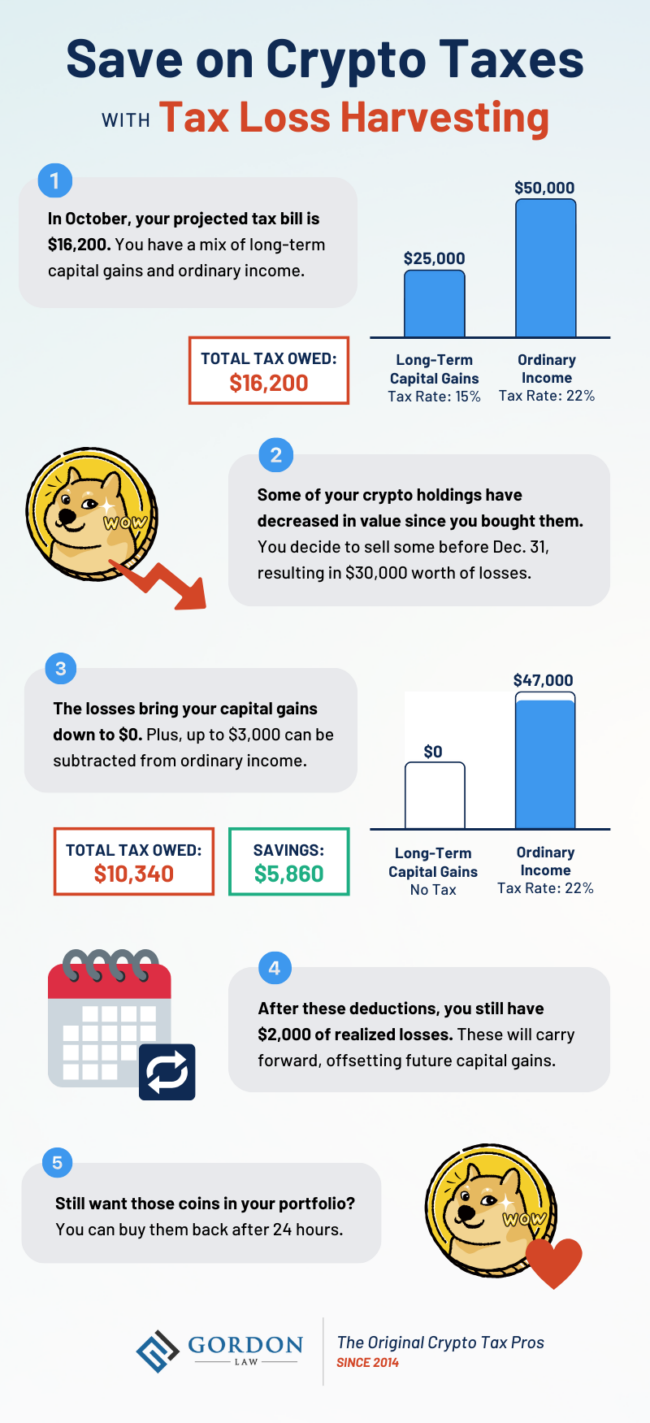

- Bring your crypto capital gains (and the resulting taxes) down to $0

- Offset other income by up to $3,000

- Carry losses forward to future years

The best part? Unlike with stocks, you can buy back your crypto assets after 24 hours, so it has a minimal effect on your portfolio.

Crypto and the Wash Sale Rule

The wash sale rule (also known as the 30-day rule) puts limitations on tax loss harvesting when it comes to stocks and securities. The IRS says that you must wait 30 days before buying the asset back. However, most cryptocurrencies and NFTs don’t have this restriction.

Currently, most digital assets are not legally defined as securities, so they’re exempt from the wash sale rule. The legislation was specifically made for stocks and securities.

The way digital assets are classified could change in the future as regulations continue to develop, so reach out to one of our crypto tax lawyers if you have any questions.

Who Can Benefit from Crypto Tax Loss Harvesting?

Any crypto investor with unrealized losses can take advantage of tax loss harvesting, but this strategy primarily helps investors in higher tax brackets.

Depending on your total income, you may already have a 0% tax rate on long-term capital gains:

- Single Filer or Married Filing Separately: Up to $44,625

- Married Filing Jointly: Up to $89,250

- Head of Household: Up to $59,750

If you fall into one of these brackets, crypto tax loss harvesting may not actually save you any money.

However, the effectiveness of crypto tax loss harvesting depends on several factors, including your total income and the mix of short-term vs long-term gains. We recommend working with a crypto tax professional for a custom analysis of your situation.

Story Time: Crypto Tax Loss Harvesting Examples

To help understand the benefits of tax loss harvesting for cryptocurrency investors, let’s look at some examples.

Scenario 1: Multi-Year Tax Savings Uncovered

One of our clients, “Jane,” asked us to check her tax loss harvesting opportunities in the fall of 2023. She had $10,000 in capital gains so far. Although her gains were relatively small, Jane had a high amount of total income, putting her in one of the highest tax brackets, so she wanted to reduce her bill as much as possible.

Using our in-house tax loss harvesting tool, Jane’s accountant identified $287,000 in potential losses. We helped her identify exactly which coins to sell in which amounts in order to maximize her savings.

Not only did Jane eliminate her capital gains taxes for the year, but she also offset $3,000 of other income (the maximum amount you can take per year). Better yet, her losses will carry forward, reducing taxes on any future gains!

After 24 hours, Jane was able to buy back the crypto she wanted to keep in her portfolio, so she didn’t damage her long-term investment strategy.

Scenario 2: He Missed Out on $120,000 in Savings

Another client (let’s call him “Brian”) was holding onto coins that had lost $600,000 in value since he bought them. Our accountants shared how Brian could harvest his losses and save $120,000 on capital gains tax.

But Brian waited too long… He didn’t pull the trigger by December 31. He paid an extra $120,000 in taxes that he could have avoided.

Don’t be like Brian. Start early, consult with a qualified crypto CPA, and take advantage of tax loss harvesting before it’s too late!

When Should I Use Crypto Tax Loss Harvesting?

The tax loss harvesting deadline is December 31 of each year. Most crypto investors wait until the last minute to harvest their losses, but we recommend starting in September or October.

If you want to pursue more aggressive tax savings, you can tax loss harvest throughout the entire year, taking advantage of market dips. Since the cryptocurrency market is so volatile, investors may have several chances during the year to take advantage of drastic price dips.

However, in order to maximize your tax loss harvesting opportunities, you need to stay on top of your crypto tax reporting.

The hardest part for crypto investors is identifying which coin has the highest cost basis compared to the current market price. Without this information, it’s nearly impossible to use tax loss harvesting effectively. Need help figuring it out? Reach out to our experienced cryptocurrency accounting team.

NFT Tax Loss Harvesting

NFTs create excellent opportunities for tax loss harvesting. Perhaps your NFTs have become worthless due to a rug pull, or maybe they’ve simply lost value in a bear market. Either way, selling your NFTs to harvest the losses is a smart move to consider.

With some “worthless” NFTs, you might find it challenging to sell the asset. What can you do when there are no buyers for your NFTs?

Tools like Unsellable NFTs and NFT Loss Harvestooor allow you to sell illiquid NFTs in order to realize a loss and lower your capital gains.

Be sure to avoid selling to yourself or to people in your social circle, as you may not be able to legally claim your losses. Look for buyers that have been audited and verified; and, ideally, talk to your tax professional to optimize your tax loss harvesting strategy! Read our NFT Tax Guide to learn more.

Want to Save on Your Next Tax Bill? We Can Help!

Whether you need help with tax loss harvesting or want to explore additional ways to pay less crypto tax, Gordon Law Group is here to help. Our cryptocurrency tax lawyers have been helping investors save money and stay compliant since 2014! Don’t hesitate to reach out if you have any questions.