The IRS has announced that new reporting requirements for cryptocurrency business transactions over $10,000 will be delayed pending further regulations. Receipt of digital asset payments will not have to be reported on Form 8300 just yet.

This comes as a relief to many businesses accepting large cryptocurrency payments—including miners, stakers, NFT creators, and full-time traders—due to concerns over their ability to comply with the law.

At Gordon Law, we’ve helped more than 1,000 cryptocurrency investors and businesses navigate complex tax regulations since 2014. Here’s what you need to know about the new $10,000 reporting requirement and Form 8300.

Understanding the $10,000 Crypto Reporting Requirement

Early this year, the crypto community was buzzing with concerns over a new reporting requirement.

On January 1, 2024, a provision of the Infrastructure Investment and Jobs Act (signed in November 2021) was set to take effect. Here’s what you need to know about the new regulation in a nutshell:

- The regulation requires businesses to report the receipt of cryptocurrency payments of $10,000 or more.

- This includes not only single transactions, but also multiple related transactions that collectively surpass the $10,000 threshold.

- The rule mandates providing detailed information for each qualifying transaction, such as the name, address, and Social Security or taxpayer identification number of the sender, as well as the transaction’s amount, date, and nature.

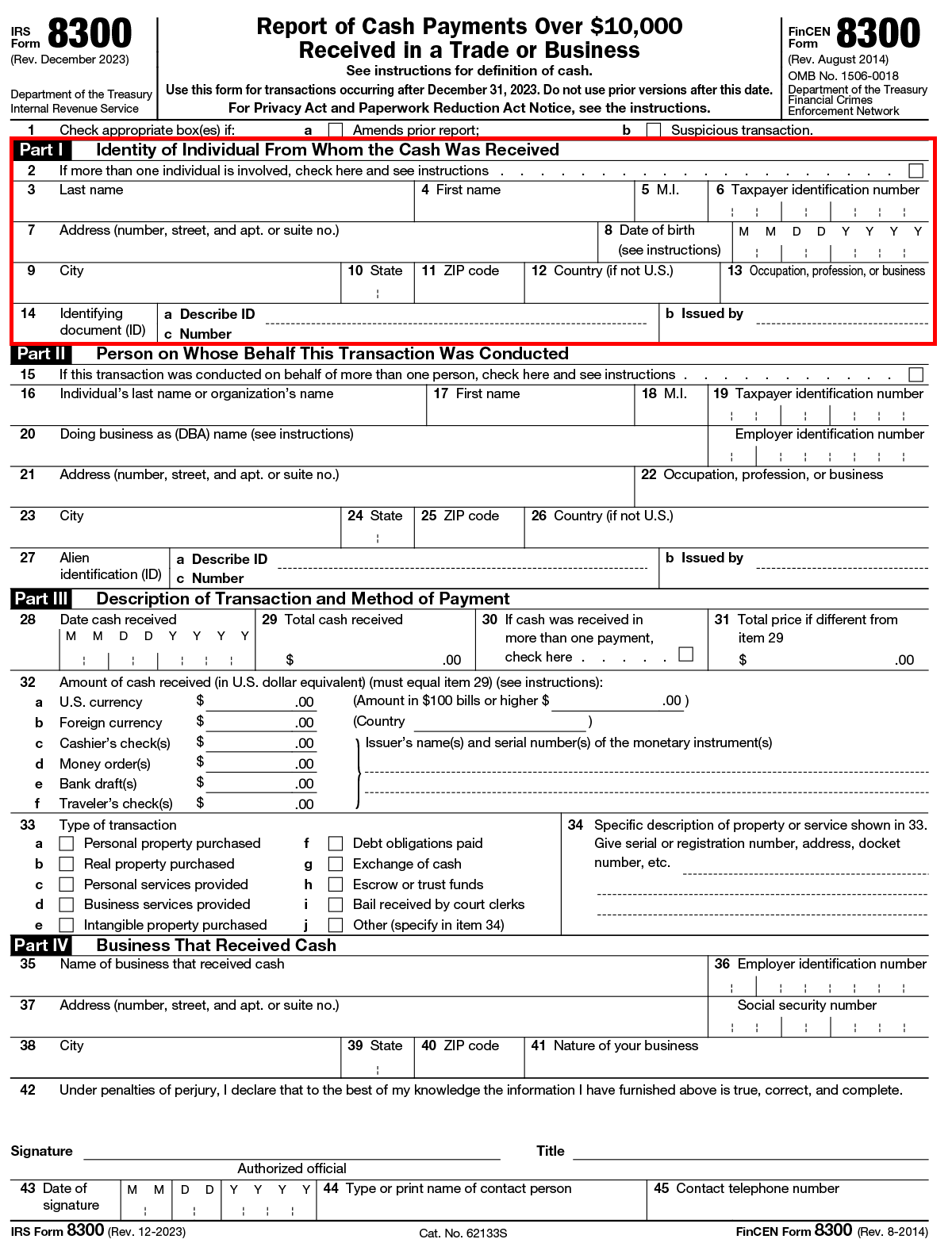

- Reports must be filed within 15 days of the transaction using Form 8300, “Report of Cash Payments Over $10,000 Received in a Trade or Business.”

This regulation aims to create transparency and assist with the enforcement of cryptocurrency tax requirements. However, there have been serious concerns about the ability of businesses to comply when it comes to crypto payments.

Tax attorney and CPA Andrew Gordon provides some background on Form 8300 and the new crypto regulation. He explains that Form 8300 has existed for many years and is used when a business receives cash of $10,000 or more.

For example, if you bought a used car from a dealership using cash, the dealership would have to report that transaction to the IRS and FinCEN using Form 8300. “It’s to get on top of money laundering and potential tax evasion. Now, it’s expanded to include crypto,” says Gordon.

Problems with Form 8300 Filing Compliance

Under the new regulation, qualifying crypto transactions must be reported by the recipient on Form 8300 within 15 days of receipt. This form requires detailed information about the sender of the payment, including the sender’s name, address, and Social Security number or taxpayer identification number.

In the world of cryptocurrency, it may be impossible to gather all this information due to the decentralized nature of the blockchain. For example, it’s common for an NFT artist to receive payment from an anonymous individual. In such cases, the artist would know nothing about the sender of the payment except an anonymous wallet address.

In addition to the question of anonymous payments, Gordon explains that it’s impossible to report cryptocurrency payments using the current form. “Looking at the Form 8300 as it is today, it’s actually not ready for us to start to disclose crypto.” The form specifies the type of payment received: U.S. currency, foreign currency, cashier’s check, money order, etc. There is no option for digital assets.

These issues have raised many concerns for cryptocurrency businesses who cannot possibly comply with the new reporting requirement.

IRS Delays Implementation of Form 8300 Reporting for Crypto

On January 16, 2024, the IRS released Announcement 2024-04, “Transitional guidance under section 6050I with respect to the reporting of information on the receipt of digital assets.” In this document, the IRS specified that digital asset payments do not need to be reported on Form 8300 until more specific regulations for digital assets have been finalized.

“The Treasury Department and the IRS intend to implement section 80603(b)(3) of the Infrastructure Act by publishing regulations specifically addressing the application of section 6050I to digital assets and by providing forms and instructions for reporting that address the inclusion of digital assets,” reads the announcement.

Who Will Be Required to Report $10,000 Crypto Transactions?

“This form is only relevant if you have a trade or business,” says Gordon. “Although it sounds like [trade or business are] these generic terms, they’re actually legal terms of art, and they describe operating an ongoing business. In the example of staking, sometimes staking could be considered a business. In many cases, it’s not.”

However, many people in the cryptocurrency industry will be required to report on Form 8300.

Gordon hopes that in addition to modifying Form 8300 to include digital assets, regulators will limit the scope of who needs to file.

“How would this form be filled out if you were staking and then you received payment of cryptocurrency? That’s a great question,” says Gordon. “In fact, myself and many practitioners think that it would be nearly impossible with staking. So there has to be a carve-out for activity like that.”

Ready to Navigate the New Crypto Reporting Landscape? Gordon Law Can Help

The new rules for cryptocurrency transactions over $10,000 mark a notable shift in financial reporting requirements. The IRS has given crypto businesses some much-needed breathing room, but it’s important to stay up to date on regulations to avoid IRS problems.

If you need help navigating these changes, our experienced cryptocurrency tax attorneys are here to guide you. Get in touch today for a confidential consultation.